import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pandas_datareader as pdr

import seaborn as sns

import yfinance as yfHerron Topic 5 - Practice for Section 04

FINA 6333 for Spring 2024

1 Practice

%precision 2

pd.options.display.float_format = '{:.2f}'.format

%config InlineBackend.figure_format = 'retina'1.1 Estimate \(\pi\) by simulating darts thrown at a dart board

Hints: Select random \(x\)s and \(y\)s such that \(-r \leq x \leq +r\) and \(-r \leq x \leq +r\). Darts are on the board if \(x^2 + y^2 \leq r^2\). The area of the circlular board is \(\pi r^2\), and the area of square around the board is \((2r)^2 = 4r^2\). The fraction \(f\) of darts on the board is the same as the ratio of circle area to square area, so \(f = \frac{\pi r^2}{4 r^2}\).

First we throw darts at the board. Darts with \(x^2 + y^2 \leq r^2\) are on the board.

def throw_darts(n=10_000, r=1, seed=42):

np.random.seed(seed)

return (

pd.DataFrame(

data=np.random.uniform(low=-r, high=r, size=2*n).reshape(n, 2),

columns=['x', 'y']

)

.assign(board=lambda x: x['x']**2 + x['y']**2 <= r**2)

.rename_axis(index='n', columns='Variable')

)throw_darts()| Variable | x | y | board |

|---|---|---|---|

| n | |||

| 0 | -0.25 | 0.90 | True |

| 1 | 0.46 | 0.20 | True |

| 2 | -0.69 | -0.69 | True |

| 3 | -0.88 | 0.73 | False |

| 4 | 0.20 | 0.42 | True |

| ... | ... | ... | ... |

| 9995 | 0.15 | 0.52 | True |

| 9996 | -0.82 | -0.01 | True |

| 9997 | 0.80 | 0.75 | False |

| 9998 | -0.91 | -0.39 | True |

| 9999 | -0.11 | -0.66 | True |

10000 rows × 3 columns

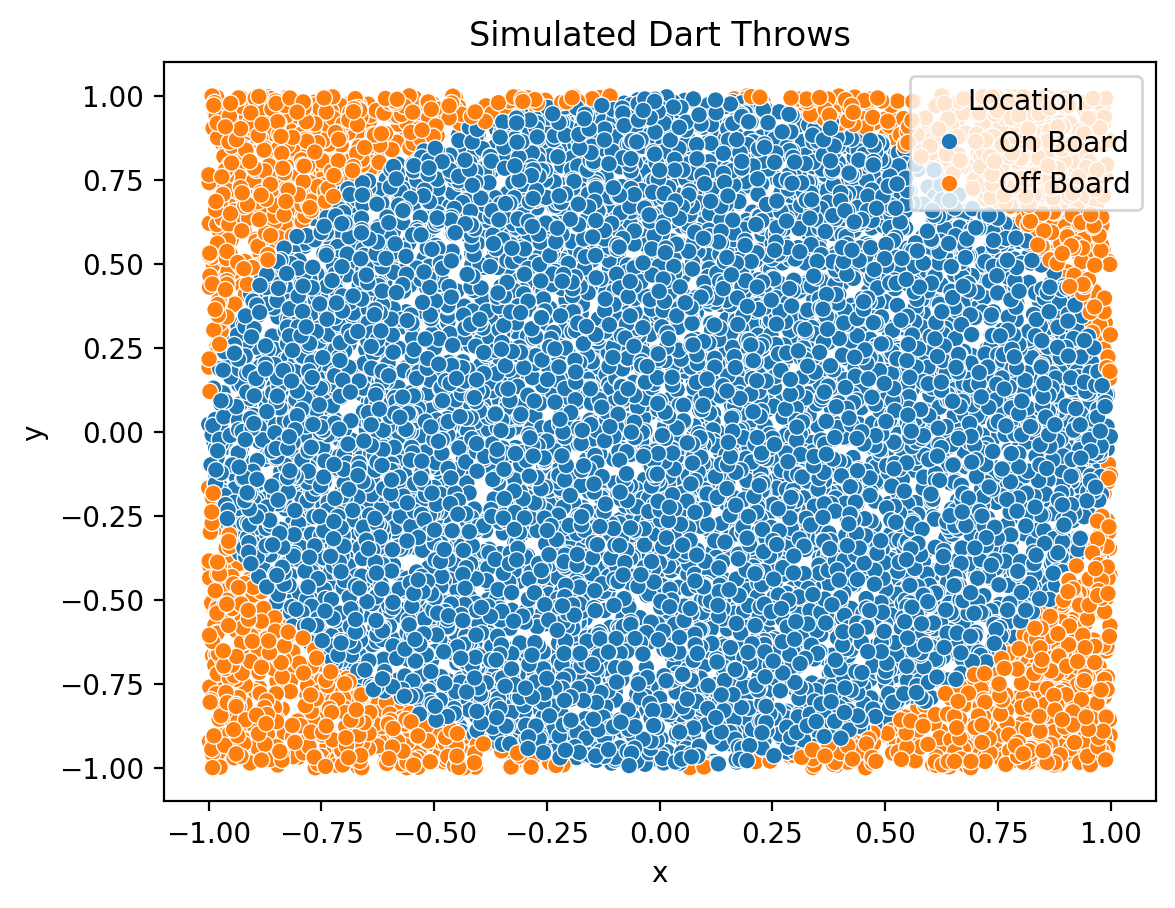

Next, we visualize these darts with a scatter plot. Seaborn’s scatterplot() helps color darts by location (i.e., on or off board). The .pipe() method lets us send the output of the .assign() method to sns.scatterplot() without assigning a temporary data frame.

(

throw_darts()

.assign(Location=lambda x: np.where(x['board'], 'On Board', 'Off Board'))

.pipe(lambda x: sns.scatterplot(data=x, x='x', y='y', hue='Location'))

)

plt.title('Simulated Dart Throws')

plt.show()

Finally, we use the hint above to estimate \(\pi\). The hint above says \(f = \frac{\pi r^2}{4 r^2}\), where \(f\) is the fraction of darts on the board. Therefore, \(\pi = \frac{4fr^2}{r^2} = 4f\).

n = 10_000

pi = 4 * throw_darts(n=n)["board"].mean()

print(f'Estimate of pi based on {n:,.0f} darts: {pi:0.4f}')Estimate of pi based on 10,000 darts: 3.1544We increase the precision of our \(\pi\) estimate by increasing the number of simulated darts \(n\).

for n in 10**np.arange(7):

pi = 4 * throw_darts(n=n)["board"].mean()

print(f'Estimate of pi based on {n:<9,.0f} darts: {pi:0.4f}')Estimate of pi based on 1 darts: 4.0000

Estimate of pi based on 10 darts: 3.2000

Estimate of pi based on 100 darts: 3.0400

Estimate of pi based on 1,000 darts: 3.1040

Estimate of pi based on 10,000 darts: 3.1544

Estimate of pi based on 100,000 darts: 3.1468

Estimate of pi based on 1,000,000 darts: 3.14201.2 Simulate your wealth \(W_T\) by randomly sampling market returns

Use monthly market returns from the French Data Library. Only invest one cash flow \(W_0\), and plot the distribution of \(W_T\).

First, we download data from the French Data Library. We convert these returns from percent to decimal to simplify compounding.

mkt = (

pdr.DataReader(

name='F-F_Research_Data_Factors_daily',

data_source='famafrench',

start='1900'

)[0]

.assign(mkt=lambda x: (x['Mkt-RF'] + x['RF']) / 100)

['mkt']

)C:\Users\r.herron\AppData\Local\Temp\ipykernel_13960\526361920.py:2: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

pdr.DataReader(Next, we write a couple of helper functions. The get_sample() function draws one random sample of n observations from returns series x. This sample provides one simulated return history.

pd.date_range<function pandas.core.indexes.datetimes.date_range(start=None, end=None, periods=None, freq=None, tz=None, normalize: 'bool' = False, name: 'Hashable | None' = None, inclusive: 'IntervalClosedType' = 'both', *, unit: 'str | None' = None, **kwargs) -> 'DatetimeIndex'>def get_sample(x, n=10_000, seed=42, start=None):

if start is None:

start = x.index[-1] + pd.offsets.BDay()

return (

x

.sample(n=n, replace=True, random_state=seed, ignore_index=True)

.set_axis(pd.date_range(start=start, periods=n, freq='B'))

.rename_axis(index='Date')

) The get_samples() function calls the get_sample() function m times to simulate m return histories. The get_samples() function combines these m return histories into one data frame.

def get_samples(x, m=100, n=10_000, seed=42, start=None):

return (

pd.concat(

objs=[get_sample(x=x, n=n, seed=seed+i, start=start) for i in range(m)],

axis=1,

keys=range(m),

names='Sample'

)

)Next, we use these helper functions to simulate 100 return histories of 10,000 trading days each.

mkts = get_samples(x=mkt, m=100, n=10_000)

mkts| Sample | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | ... | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2024-03-01 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | -0.00 | 0.00 | -0.01 | 0.00 | ... | 0.01 | 0.01 | 0.00 | 0.01 | 0.00 | 0.00 | -0.00 | -0.01 | -0.01 | 0.00 |

| 2024-03-04 | 0.01 | -0.00 | 0.00 | 0.01 | 0.00 | -0.01 | -0.01 | 0.01 | 0.00 | -0.01 | ... | -0.00 | 0.00 | 0.01 | -0.02 | 0.00 | 0.01 | 0.01 | 0.01 | -0.01 | -0.01 |

| 2024-03-05 | -0.03 | -0.00 | -0.01 | -0.03 | -0.00 | 0.02 | -0.00 | 0.00 | -0.01 | -0.01 | ... | 0.00 | -0.00 | 0.01 | -0.02 | -0.01 | 0.01 | -0.00 | 0.00 | -0.00 | 0.01 |

| 2024-03-06 | -0.00 | -0.00 | -0.01 | -0.00 | 0.01 | 0.01 | 0.00 | -0.02 | 0.00 | -0.01 | ... | 0.01 | -0.01 | 0.00 | 0.00 | 0.00 | -0.02 | -0.02 | 0.00 | -0.00 | 0.01 |

| 2024-03-07 | -0.00 | -0.00 | -0.00 | -0.00 | -0.01 | -0.00 | 0.01 | 0.01 | -0.00 | 0.01 | ... | 0.00 | -0.00 | 0.01 | -0.01 | -0.01 | -0.03 | -0.00 | -0.01 | -0.03 | -0.00 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2062-06-23 | -0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | -0.01 | 0.00 | -0.00 | 0.01 | ... | -0.01 | -0.01 | 0.00 | 0.00 | -0.00 | -0.07 | 0.01 | 0.02 | -0.00 | -0.00 |

| 2062-06-26 | -0.00 | 0.01 | -0.00 | 0.01 | 0.00 | -0.01 | 0.01 | 0.00 | -0.00 | -0.00 | ... | 0.00 | -0.00 | -0.01 | -0.00 | -0.01 | 0.00 | 0.01 | 0.01 | 0.03 | -0.01 |

| 2062-06-27 | -0.01 | -0.01 | 0.02 | -0.04 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 | 0.01 | ... | 0.00 | -0.00 | -0.01 | 0.01 | 0.00 | 0.01 | 0.01 | 0.01 | 0.00 | 0.01 |

| 2062-06-28 | -0.01 | -0.01 | 0.00 | -0.00 | -0.01 | -0.00 | 0.04 | 0.00 | -0.00 | -0.00 | ... | 0.02 | -0.00 | -0.01 | -0.01 | -0.00 | 0.01 | 0.00 | 0.01 | -0.00 | -0.01 |

| 2062-06-29 | -0.00 | 0.00 | -0.01 | 0.01 | -0.01 | 0.00 | -0.01 | -0.01 | -0.01 | 0.00 | ... | -0.00 | 0.01 | 0.01 | 0.01 | -0.00 | 0.00 | -0.01 | -0.02 | 0.01 | -0.01 |

10000 rows × 100 columns

We compound daily returns \(R_t\) to find future wealth \(W_T\), so \(W_T = W_0 \times (1 + R_1) \times (1 + R_2) \times \cdots \times (1 + R_T)\). We use the .cumprod() method to compound the daily returns in data frame mkts.

W_0 = 1_000_000

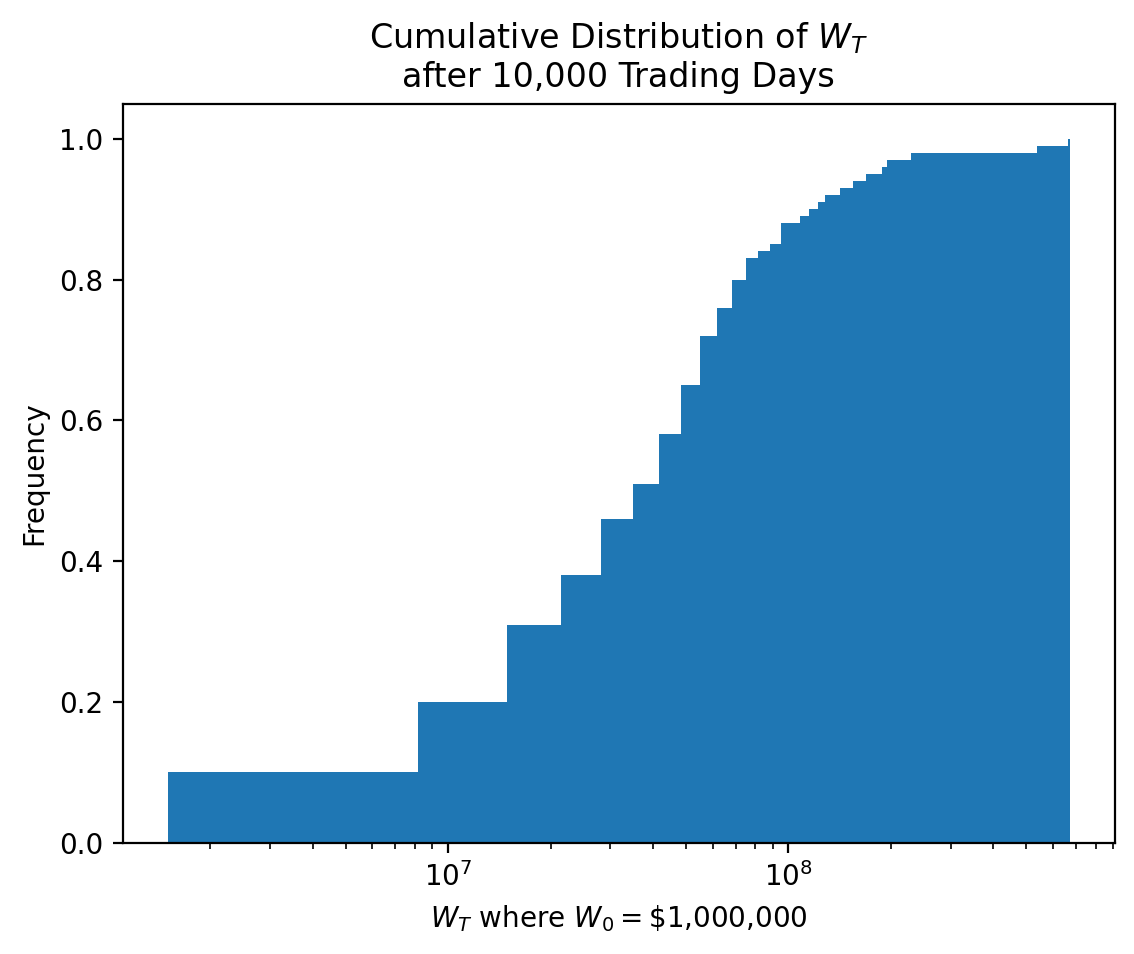

W_t = W_0 * mkts.add(1).cumprod()We visualize terminal wealth \(W_T\) with a cumulative distribution plot.

W_t.iloc[-1].plot(kind='hist', density=True, cumulative=True, bins=100)

plt.semilogx()

plt.xlabel(r'$W_T$ where $W_0 = $' + f'\\${W_0:,.0f}')

plt.title(r'Cumulative Distribution of $W_T$' + f'\nafter {W_t.shape[0]:,.0f} Trading Days')

plt.show()

The plot above shows the cumulative distribution of \(W_T\), suggesting we expect \(W_T\) greater than about 20 million dollars for about 75% of samples. The plot above may be difficult to read and interpret because \(W_T\) has large outliers. The .describe() method provides few salient values of \(W_T\). We convert \(W_T\) from dollars to millions of dollars with .div(1_000_000).

W_t.iloc[-1].div(1_000_000).describe()count 100.00

mean 61.07

std 90.71

min 1.50

25% 18.12

50% 41.47

75% 66.93

max 669.23

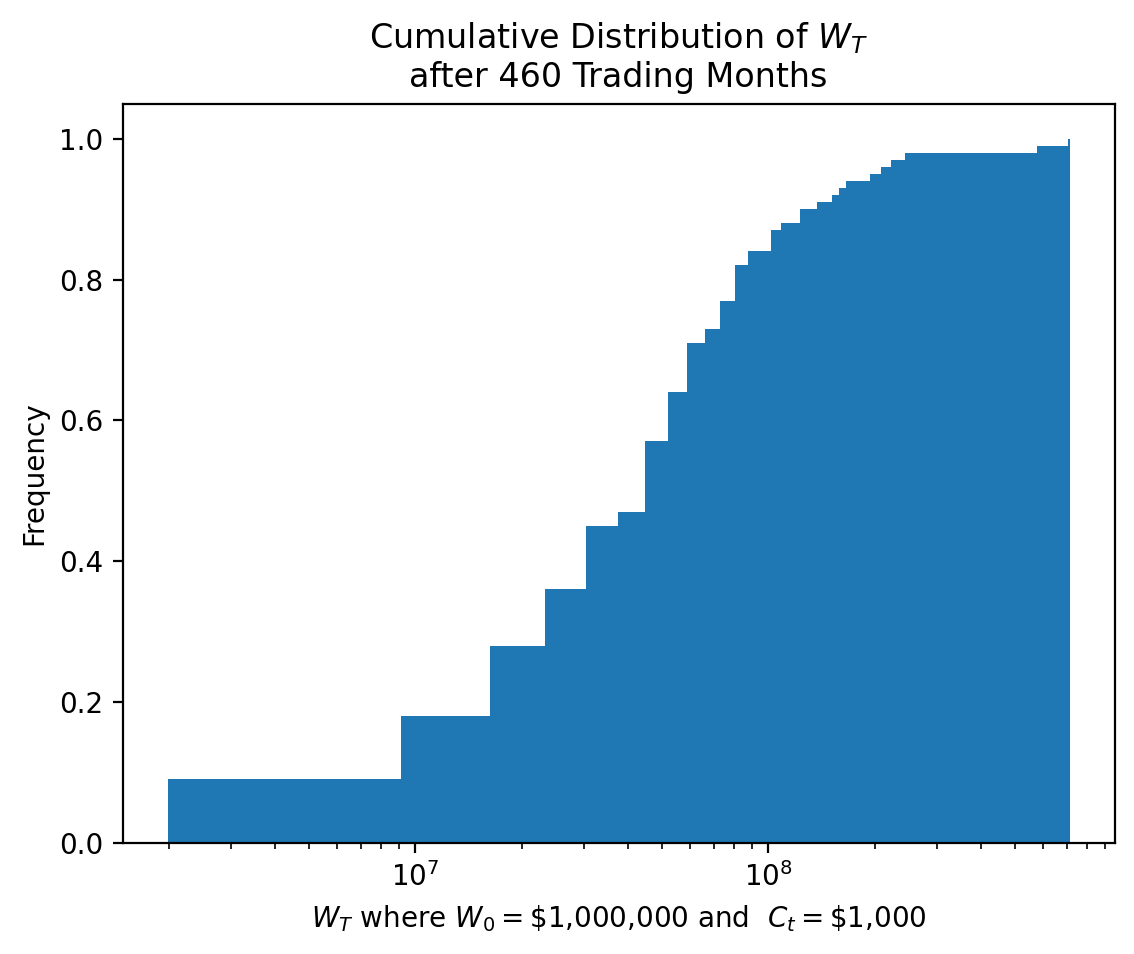

Name: 2062-06-29 00:00:00, dtype: float641.3 Repeat the exercise above but add end-of-month investments \(C_t\)

We can use the same data frame mkts of simulated market returns. However, need to consider end-of-month investments of \(C_t\). The easiest approach is to aggregate the daily market returns in mkts to monthly market returns in data frame mkts_m.

mkts_m = (

mkts

.add(1)

.resample(rule='M', kind='period')

.prod()

.sub(1)

)The wealth at time \(t\) is \(W_t\) and depends on:

- The wealth at the end of the previous month \(W_{t-1}\)

- The return over the previous month \(R_t\) (recall we label returns by their right edge)

- The end-of-month investment \(C_t\)

Putting it all togther: \(W_t = W_{t-1} \times (1 + R_t) + C_t\)

We have to loop over the monthly returns in mkts_m because we have to combine compounded returns and cash flows. The iterrows() methods provides an easy way to iterate (loop) over the rows in mkts_m.

C_t = 1_000

W_0 = 1_000_000

W_last = W_0

W_t = []

for d, m in mkts_m.iterrows():

W_last = (1 + m) * W_last + C_t

W_t.append(W_last)

W_t = pd.concat(objs=W_t, axis=1, keys=mkts_m.index).transpose()We repeat the cumulative distribution of wealth plot and descriptive statistics from above.

W_t.iloc[-1].plot(kind='hist', density=True, cumulative=True, bins=100)

plt.semilogx()

plt.xlabel(

r'$W_T$ where $W_0 = $' + f'\\${W_0:,.0f}' +

r' and $C_t = $' + f'\\${C_t:,.0f}'

)

plt.title(r'Cumulative Distribution of $W_T$' + f'\nafter {W_t.shape[0]:,.0f} Trading Months')

plt.show()

W_t.iloc[-1].div(1_000_000).describe()count 100.00

mean 67.84

std 97.55

min 1.99

25% 21.21

50% 46.54

75% 75.92

max 713.85

Name: 2062-06, dtype: float64The plot above shows the cumulative distribution of \(W_T\), suggesting we expect \(W_T\) greater than about 20 million dollars for about 75% of samples. Note, even though we deposit $1,000 per month for almost 40 years, we do not gain much wealth over the previous example with only a lump sum! Start saving early!