import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pandas_datareader as pdr

import seaborn as sns

import statsmodels.formula.api as smf

import yfinance as yfHerron Topic 3 - Multifactor Models

FINA 6333 for Spring 2024

This notebook covers multifactor models, emphasizing the capital asset pricing model (CAPM) and the Fama-French three-factor model (FF3). Ivo Welch provides a high-level review of the CAPM and multifactor models in Chapter 10 of his free Corporate Finance textbook. The Wikipedia page for the CAPM is surprisingly good and includes its assumptions and shortcomings.

%precision 4

pd.options.display.float_format = '{:.4f}'.format

%config InlineBackend.figure_format = 'retina'1 The Capital Asset Pricing Model (CAPM)

The CAPM explains the relation between non-diversifiable risk and expected return and has applications throughout finance. We use the CAPM to estimate expected rates of return in investment analysis, estimate costs of capital in corporate finance, and assemble portfolios with a given risk-return tradeoff in portfolio management. The formula for the CAPM is \(E(r_i) = r_f + \beta_i [E(r_M) - r_f]\), where:

- \(r_f\) is the risk-free rate of return,

- \(\beta_i\) is the measure of non-diversifiable risk for asset \(i\), and

- \(E(r_M)\) is the expected rate of return on the market.

The value-weighted mean of all \(\beta_i\)s is 1 by construction, but a range of \(\beta_i\)s is possible:

- \(\beta_i < -1\): Asset \(i\) moves in the opposite direction as the market, in larger magnitudes

- \(-1 \leq \beta_i < 0\): Asset \(i\) moves in the opposite direction as the market

- \(\beta_i = 0\): Asset \(i\) has no correlation between with the market

- \(0 < \beta_i \leq 1\): Asset \(i\) moves in the same direction as the market, in smaller magnitudes

- \(\beta_i = 1\): Asset \(i\) moves in the same direction with the same magnitude as the market

- \(\beta_i > 1\): Asset \(i\) moves in the same direction as the market, in larger magnitudes

We will follow Bodie, Kane, and Marcus’s notation:

- Lowercase \(r_i\) is the raw return on asset \(i\)

- Uppercase \(R_i\) is the excess return on asset \(i\)

- So, \(R_i = r_i - r_f\) and \(R_M = r_M - r_f\)

1.1 \(\beta\) Estimation

We can use three approaches to estimate CAPM \(\beta_i\)s:

- Use the covariance and variance of excess returns: \(\beta_i = \frac{Cov(r_i - r_f, r_M - r_f)}{Var(r_M - r_f)}\)

- Use the correlation and standard deviations of excess returns: \(\beta_i = \rho_{i, M} \frac{\sigma_i}{\sigma_M}\)

- Use a linear regression of asset excess returns \(r_i-r_f\) on market excess returns \(r_M-r_f\)

The first two approaches are computationally faster. However, the third approach also estimates the intercept \(\alpha_i\) and several goodness-of-fit statistics. We can use Apple (AAPL) to convince ourselves these three approaches are equivalent.

Note, we will leave returns in percent to make it easier to interpret our regression output! Leaving returns in percent does not affect \(\beta\) estimates (slopes) but makes \(\alpha\) estimates (intercepts) easier to interpret because they are in percents instead of decimals.

aapl = (

yf.download(tickers='AAPL')

.rename_axis(columns='Variable')

)

aapl.tail()[*********************100%%**********************] 1 of 1 completed| Variable | Open | High | Low | Close | Adj Close | Volume |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2024-03-22 | 171.7600 | 173.0500 | 170.0600 | 172.2800 | 172.2800 | 71106600 |

| 2024-03-25 | 170.5700 | 171.9400 | 169.4500 | 170.8500 | 170.8500 | 54288300 |

| 2024-03-26 | 170.0000 | 171.4200 | 169.5800 | 169.7100 | 169.7100 | 57388400 |

| 2024-03-27 | 170.4100 | 173.6000 | 170.1100 | 173.3100 | 173.3100 | 60273300 |

| 2024-03-28 | 171.7500 | 172.2300 | 170.5100 | 171.4800 | 171.4800 | 65623100 |

ff = (

pdr.DataReader(

name='F-F_Research_Data_Factors_daily',

data_source='famafrench',

start='1900',

)

)

ff[0].tail()C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\3958803354.py:2: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

pdr.DataReader(| Mkt-RF | SMB | HML | RF | |

|---|---|---|---|---|

| Date | ||||

| 2024-01-25 | 0.4600 | 0.0400 | 0.5600 | 0.0220 |

| 2024-01-26 | -0.0200 | 0.4000 | -0.2700 | 0.0220 |

| 2024-01-29 | 0.8500 | 1.0700 | -0.5900 | 0.0220 |

| 2024-01-30 | -0.1300 | -1.2600 | 0.8400 | 0.0220 |

| 2024-01-31 | -1.7400 | -0.9200 | -0.3000 | 0.0220 |

aapl = (

aapl

.join(ff[0])

.rename(columns={'Mkt-RF': 'RM', 'RF': 'rf'})

.assign(

ri=lambda x: x['Adj Close'].pct_change().mul(100),

Ri = lambda x: x['ri'] - x['rf'],

rM=lambda x: x['RM'] + x['rf']

)

)

aapl.head()| Open | High | Low | Close | Adj Close | Volume | RM | SMB | HML | rf | ri | Ri | rM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||

| 1980-12-12 | 0.1283 | 0.1289 | 0.1283 | 0.1283 | 0.0992 | 469033600 | 1.3800 | -0.0100 | -1.0500 | 0.0590 | NaN | NaN | 1.4390 |

| 1980-12-15 | 0.1222 | 0.1222 | 0.1217 | 0.1217 | 0.0940 | 175884800 | 0.1100 | 0.2500 | -0.4600 | 0.0590 | -5.2170 | -5.2760 | 0.1690 |

| 1980-12-16 | 0.1133 | 0.1133 | 0.1127 | 0.1127 | 0.0871 | 105728000 | 0.7100 | -0.7500 | -0.4700 | 0.0590 | -7.3398 | -7.3988 | 0.7690 |

| 1980-12-17 | 0.1155 | 0.1161 | 0.1155 | 0.1155 | 0.0893 | 86441600 | 1.5200 | -0.8600 | -0.3400 | 0.0590 | 2.4751 | 2.4161 | 1.5790 |

| 1980-12-18 | 0.1189 | 0.1194 | 0.1189 | 0.1189 | 0.0919 | 73449600 | 0.4100 | 0.2200 | 1.2600 | 0.0590 | 2.8992 | 2.8402 | 0.4690 |

1.1.1 Covariance and Variance Approach to Estimate \(\beta\)

vcv = aapl[['Ri', 'RM']].dropna().cov()

vcv| Ri | RM | |

|---|---|---|

| Ri | 7.8421 | 1.5508 |

| RM | 1.5508 | 1.2312 |

print(f"Apple beta from cov/var: {vcv.loc['Ri', 'RM'] / vcv.loc['RM', 'RM']:0.4f}")Apple beta from cov/var: 1.25961.1.2 Correlation and Standard Deviation Approach to Estimate \(\beta\)

_ = aapl[['Ri', 'RM']].dropna()

rho = _.corr()

sigma = _.std()

print(f'rho:\n{rho}\n\nsigma:\n{sigma}')rho:

Ri RM

Ri 1.0000 0.4991

RM 0.4991 1.0000

sigma:

Ri 2.8004

RM 1.1096

dtype: float64print(f"Apple beta from rho and sigmas: {rho.loc['Ri', 'RM'] * sigma.loc['Ri'] / sigma.loc['RM']:0.4f}")Apple beta from rho and sigmas: 1.25961.1.3 Linear Regression Approach to Estimate \(\beta\)

We will use the statsmodels package to estimate linear regressions. I typically use the formula application programming interface (API).

With statsmodels (and most Python model estimation packages), we have three steps:

- Specify the model with the

smf.ols()function - Fit the model with the

.fit()method - Summarize the model with the

.summary()method

model = smf.ols(formula='Ri ~ RM', data=aapl)

fit = model.fit()

summary = fit.summary()

summary| Dep. Variable: | Ri | R-squared: | 0.249 |

| Model: | OLS | Adj. R-squared: | 0.249 |

| Method: | Least Squares | F-statistic: | 3606. |

| Date: | Fri, 29 Mar 2024 | Prob (F-statistic): | 0.00 |

| Time: | 08:15:40 | Log-Likelihood: | -25067. |

| No. Observations: | 10873 | AIC: | 5.014e+04 |

| Df Residuals: | 10871 | BIC: | 5.015e+04 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

| Intercept | 0.0514 | 0.023 | 2.207 | 0.027 | 0.006 | 0.097 |

| RM | 1.2596 | 0.021 | 60.049 | 0.000 | 1.218 | 1.301 |

| Omnibus: | 3230.837 | Durbin-Watson: | 1.916 |

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 334498.501 |

| Skew: | -0.379 | Prob(JB): | 0.00 |

| Kurtosis: | 30.162 | Cond. No. | 1.11 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

We can recover the coefficient estimates from the fit object’s params attribute.

fit.paramsIntercept 0.0514

RM 1.2596

dtype: float64print(f"Apple beta from linear regression: {fit.params['RM']:0.4f}")Apple beta from linear regression: 1.2596We can chain these operations, but it often makes sense to save the intermediate results to model and fit objects.

smf.ols('Ri ~ RM', aapl).fit().summary()| Dep. Variable: | Ri | R-squared: | 0.249 |

| Model: | OLS | Adj. R-squared: | 0.249 |

| Method: | Least Squares | F-statistic: | 3606. |

| Date: | Fri, 29 Mar 2024 | Prob (F-statistic): | 0.00 |

| Time: | 08:16:28 | Log-Likelihood: | -25067. |

| No. Observations: | 10873 | AIC: | 5.014e+04 |

| Df Residuals: | 10871 | BIC: | 5.015e+04 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

| Intercept | 0.0514 | 0.023 | 2.207 | 0.027 | 0.006 | 0.097 |

| RM | 1.2596 | 0.021 | 60.049 | 0.000 | 1.218 | 1.301 |

| Omnibus: | 3230.837 | Durbin-Watson: | 1.916 |

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 334498.501 |

| Skew: | -0.379 | Prob(JB): | 0.00 |

| Kurtosis: | 30.162 | Cond. No. | 1.11 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

1.2 How to Visualize \(\beta\)

We can visualize \(\beta\) as a scatterplot of Ri versus RM, where \(\beta\) is the slope of the best-fit line. We can use the seaborn package’s regplot() to add this best-fit line. We can write three functions to more easily make pretty plots.

def get_beta(x):

vcv = x.dropna().cov()

beta = vcv.loc['Ri', 'RM'] / vcv.loc['RM', 'RM']

return r'$\beta=$' + f'{beta: 0.4f}'def get_dates(x):

y = x.dropna()

return f'from {y.index[0]:%b %d, %Y} to {y.index[-1]:%b %d, %Y}'def plot_beta(x, freq, name):

sns.regplot(

data=x,

x='RM',

y='Ri',

scatter_kws={'alpha': 0.1},

line_kws={'label': x.pipe(get_beta)}

)

plt.legend()

plt.xlabel(f'Market {freq} Excess Return (%)')

plt.ylabel(f'Stock {freq} Excess Return (%)')

plt.title(

r'$\beta$ Plot with ' +

f'{freq} Excess Returns for {name}' +

'\n' +

x.pipe(get_dates)

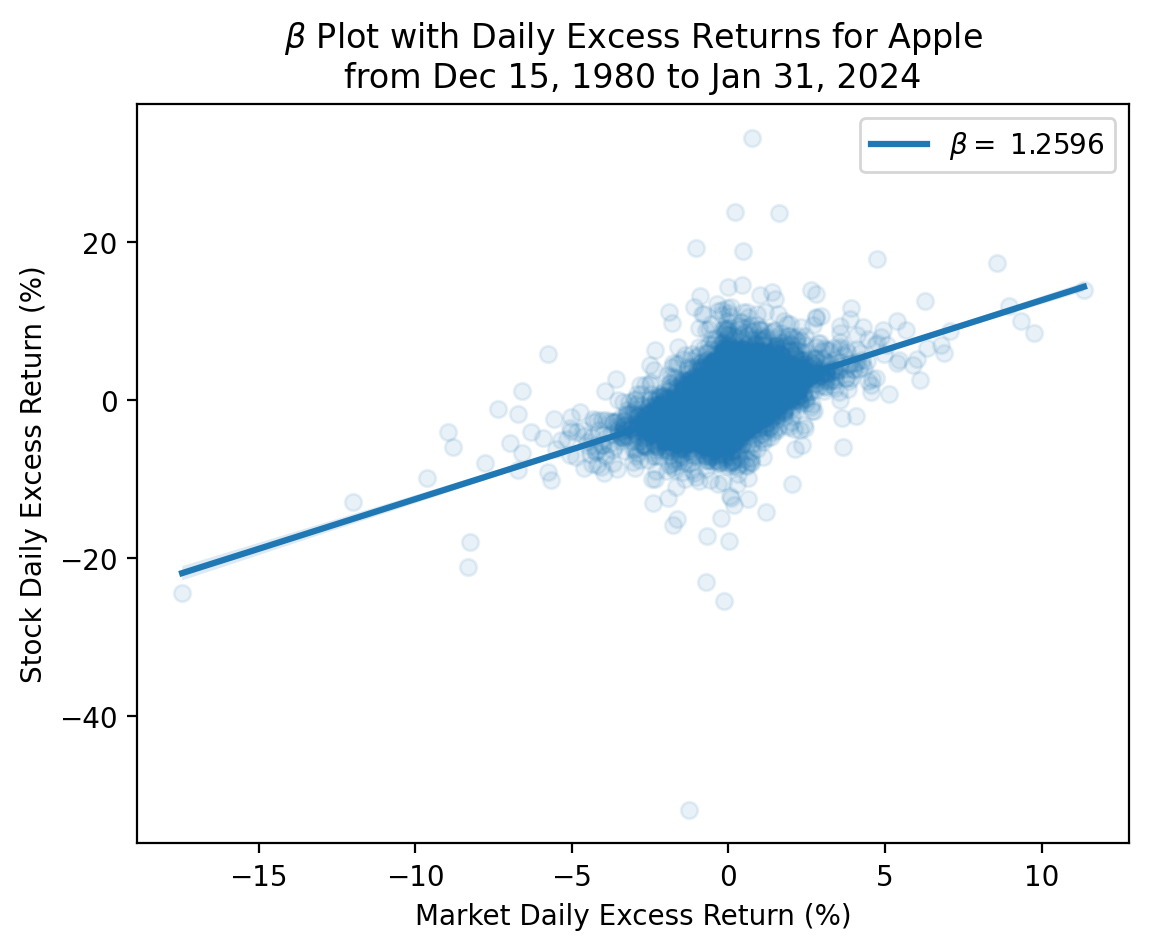

)(

aapl

[['Ri', 'RM']]

.dropna()

.pipe(plot_beta, freq='Daily', name='Apple')

)

We see a strong relation between Apple and market excess returns, but there is a lot of unexplained variation in Apple excess returns because Apple has changed a lot over the past 45 years! The best practice is to estimate \(\beta\) with one to three years of daily data.

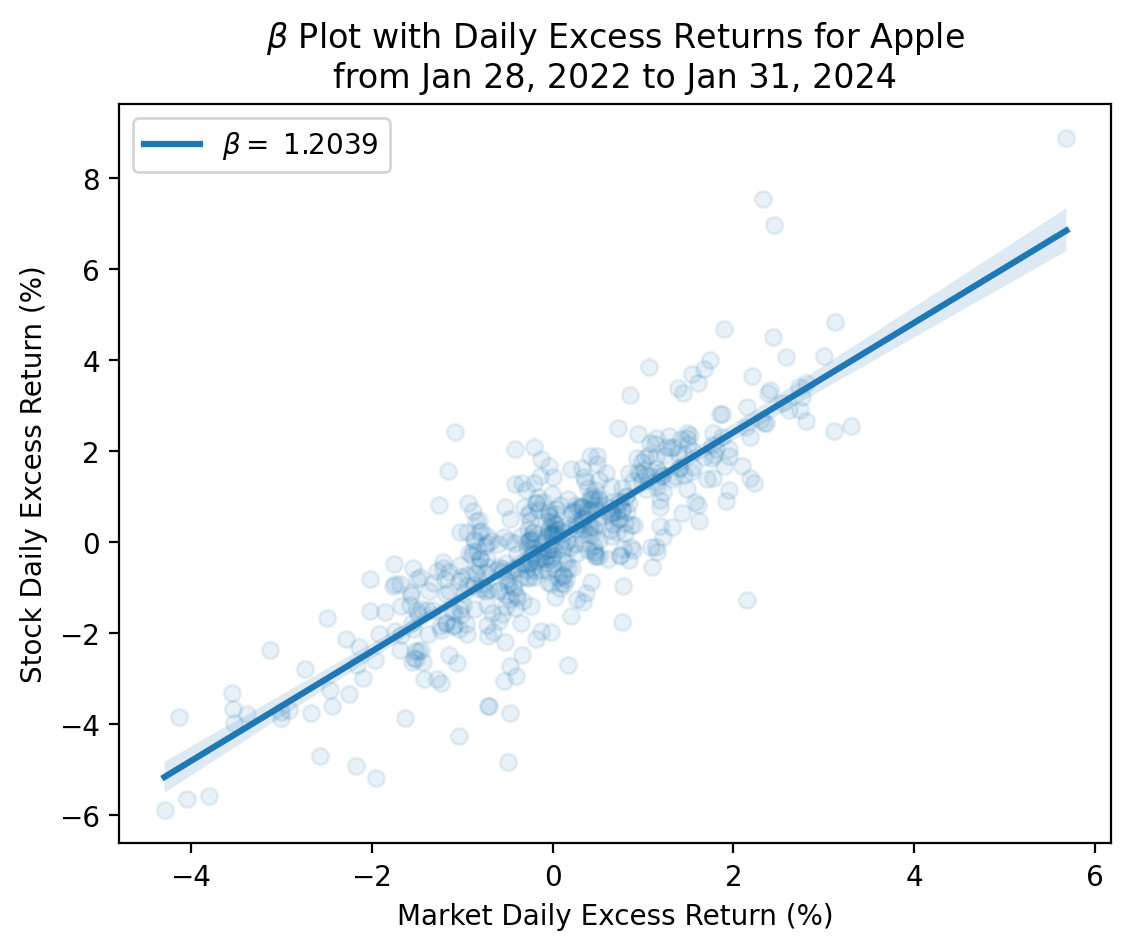

(

aapl

[['Ri', 'RM']]

.dropna()

.iloc[-504:]

.pipe(plot_beta, freq='Daily', name='Apple')

)

1.3 The Security Market Line (SML)

The SML visualizes the CAPM. We can visualize \(E(r_i) = r_f + \beta_i [E(r_M) - r_f]\) as \(y = b + xm\), where:

- The equity premium \(E(r_M) - r_f\) is the slope \(m\) of the SML

- The risk-free rate of return \(r_f\) is its intercept \(b\) of the SML

We will explore the SML more in the practice notebook.

1.4 How well does the CAPM work?

The CAPM appears to work well as a single-period model. We can see this with portfolios formed on \(\beta\) from Ken French.

ff_beta = pdr.DataReader(

name='Portfolios_Formed_on_BETA',

data_source='famafrench',

start='1900'

)C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\1792222927.py:1: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

ff_beta = pdr.DataReader(

C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\1792222927.py:1: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

ff_beta = pdr.DataReader(

C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\1792222927.py:1: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

ff_beta = pdr.DataReader(

C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\1792222927.py:1: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

ff_beta = pdr.DataReader(

C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\1792222927.py:1: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

ff_beta = pdr.DataReader(

C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\1792222927.py:1: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

ff_beta = pdr.DataReader(

C:\Users\r.herron\AppData\Local\Temp\ipykernel_25232\1792222927.py:1: FutureWarning: The argument 'date_parser' is deprecated and will be removed in a future version. Please use 'date_format' instead, or read your data in as 'object' dtype and then call 'to_datetime'.

ff_beta = pdr.DataReader(print(ff_beta['DESCR'])Portfolios Formed on BETA

-------------------------

This file was created by CMPT_BETA_RETS using the 202401 CRSP database. It contains value- and equal-weighted returns for portfolios formed on BETA. The portfolios are constructed at the end of June. Beta is estimated using monthly returns for the past 60 months (requiring at least 24 months with non-missing returns). Beta is estimated using the Scholes-Williams method. Annual returns are from January to December. Missing data are indicated by -99.99 or -999. The break points include utilities and include financials. The portfolios include utilities and include financials. Copyright 2024 Kenneth R. French

0 : Value Weighted Returns -- Monthly (727 rows x 15 cols)

1 : Equal Weighted Returns -- Monthly (727 rows x 15 cols)

2 : Value Weighted Returns -- Annual from January to December (60 rows x 15 cols)

3 : Equal Weighted Returns -- Annual from January to December (60 rows x 15 cols)

4 : Number of Firms in Portfolios (727 rows x 15 cols)

5 : Average Firm Size (727 rows x 15 cols)

6 : Value-Weighted Average of Prior Beta (61 rows x 15 cols)This file contains seven data frames. We want the data frame at [2], which contains the annual returns on two sets of portfolios formed on the previous year’s \(\beta\)s.

ff_beta[2].head()| Lo 20 | Qnt 2 | Qnt 3 | Qnt 4 | Hi 20 | Lo 10 | Dec 2 | Dec 3 | Dec 4 | Dec 5 | Dec 6 | Dec 7 | Dec 8 | Dec 9 | Hi 10 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||

| 1964 | 16.8700 | 19.7500 | 17.6600 | 8.7300 | 12.5500 | 24.7000 | 13.5900 | 20.2700 | 19.0100 | 19.7900 | 15.6800 | 9.7900 | 8.2300 | 13.6000 | 11.6600 |

| 1965 | 8.7200 | 6.9800 | 15.4000 | 24.8800 | 49.6700 | 12.4400 | 6.7600 | 10.0200 | 5.2500 | 13.7100 | 17.1100 | 20.7000 | 28.2800 | 42.0700 | 57.7300 |

| 1966 | -9.2500 | -12.1700 | -9.1000 | -2.7300 | -2.2000 | -9.4300 | -9.4400 | -12.5700 | -12.1600 | -7.5000 | -10.5600 | -6.2200 | 0.1800 | -3.3100 | -0.9400 |

| 1967 | 13.4300 | 22.0600 | 31.9500 | 42.7900 | 51.1500 | 8.9200 | 18.6400 | 22.7900 | 21.6500 | 31.1100 | 34.1600 | 40.5700 | 44.4000 | 41.6100 | 59.7800 |

| 1968 | 15.8100 | 9.1200 | 13.6400 | 14.4300 | 24.2400 | 18.4800 | 12.8400 | 14.5100 | 5.8400 | 12.6600 | 14.7500 | 19.0800 | 10.5400 | 23.2500 | 25.2900 |

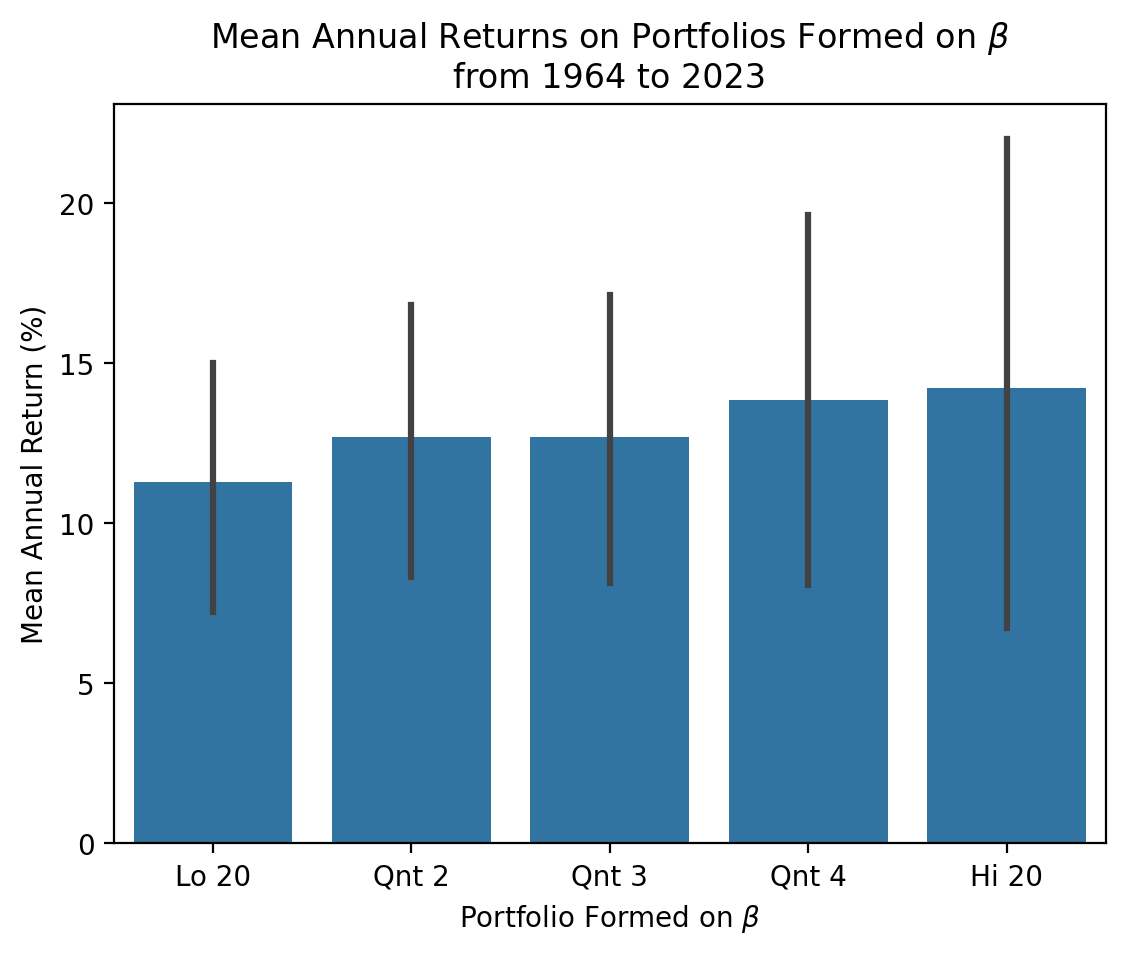

We can plot the mean annual return on each of the five portfolios in the first set of portflios. We do not need to annualize these numbers because they are the means of annual returns. The vertical black bars indicate the 95% confidence intervals for our mean annual return estimates.

_ = (

ff_beta

[2]

.iloc[:, :5]

.rename_axis(columns='Portfolio')

)

sns.barplot(

data=_.stack().to_frame('Return').reset_index(),

x='Portfolio',

y='Return'

)

plt.xlabel(r'Portfolio Formed on $\beta$')

plt.ylabel('Mean Annual Return (%)')

plt.title(

r'Mean Annual Returns on Portfolios Formed on $\beta$' +

'\n' +

f'from {_.index[0]} to {_.index[-1]}'

)

plt.show()

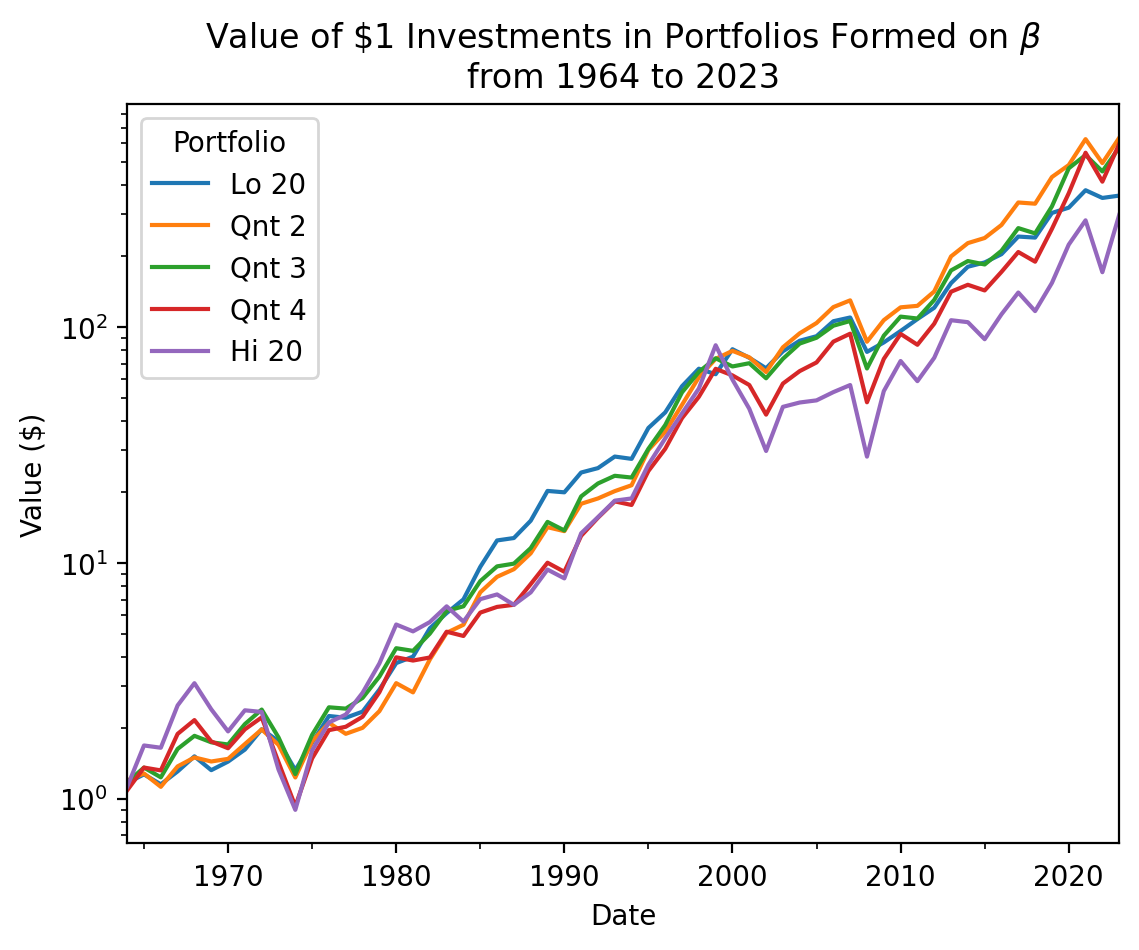

We can think of the plot above as a binned plot of the SML. The x-axis above is an ordinal measure of \(\beta\), and the y-axis above is the mean return. Recall the slope of the SML is the market risk premium. If the market risk premium is too low, then high \(\beta\) stocks do not have high enough returns. We can see this failure of the CAPM by plotting long-term or cumulative returns on these five portfolios.

_ = (

ff_beta

[2]

.iloc[:, :5]

.rename_axis(columns='Portfolio')

)

_.div(100).add(1).cumprod().plot()

plt.semilogy()

plt.ylabel('Value ($)')

plt.title(

r'Value of \$1 Investments in Portfolios Formed on $\beta$' +

'\n' +

f'from {_.index[0]} to {_.index[-1]}'

)

plt.show()

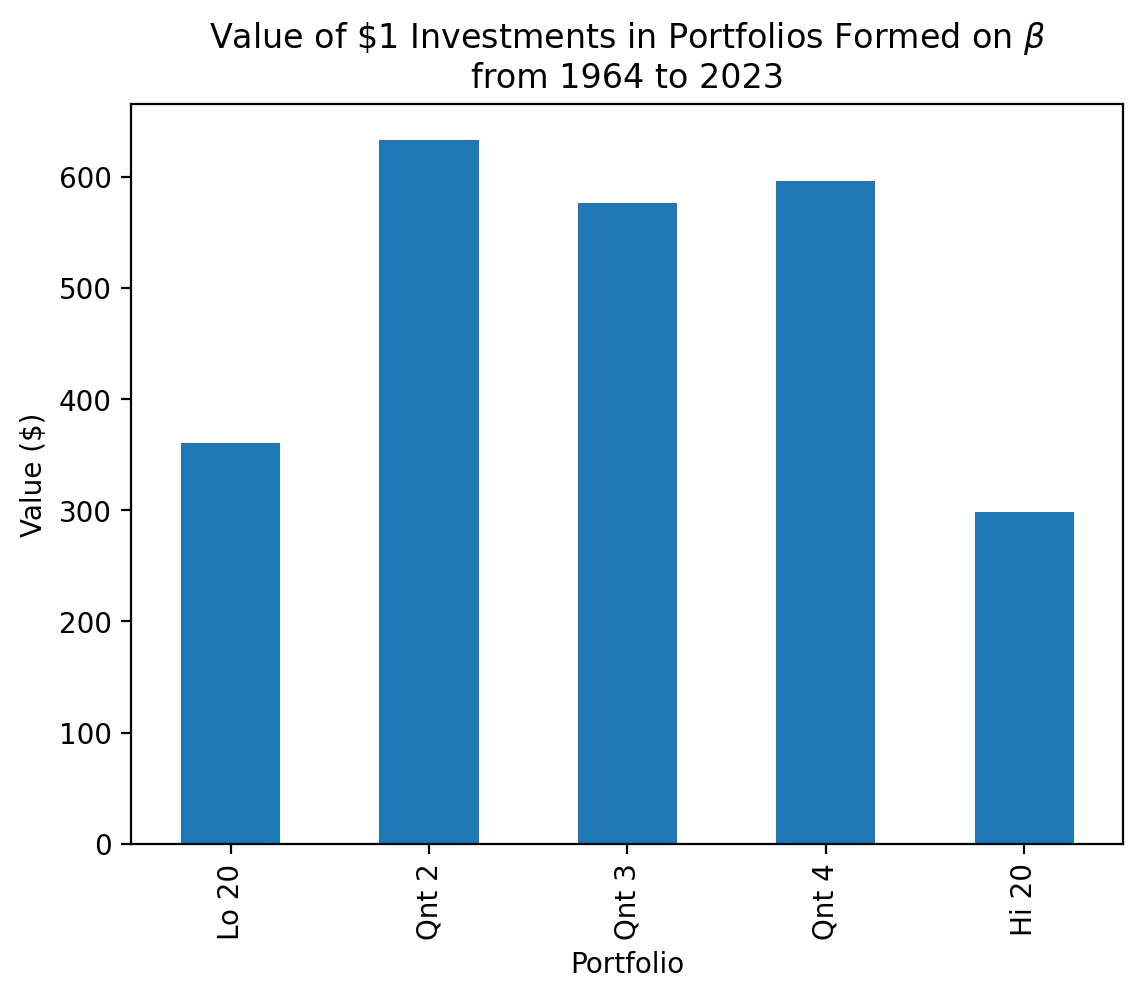

In the plot above, the highest-\(\beta\) portfolio has the lowest cumulative returns! The log scale masks a lot of variation, too!

_ = (

ff_beta

[2]

.iloc[:, :5]

.rename_axis(columns='Portfolio')

)

_.div(100).add(1).prod().plot(kind='bar')

plt.ylabel('Value ($)')

plt.title(

r'Value of \$1 Investments in Portfolios Formed on $\beta$' +

'\n' +

f'from {_.index[0]} to {_.index[-1]}'

)

plt.show()

If the CAPM does not work well, especially over the horizons we use it for (e.g., capital budgeting), why do we continue to learn it?

- The CAPM works well across asset classes. We will explore this more in the practice notebook.

- The CAPM intuition that diversification matters is correct and important

- The CAPM assigns high costs of capital to high-\(\beta\) projects (i.e., high-risk projects), which is a hidden benefit

- In practice, everyone uses the CAPM

Ivo Welch provides a more complete discussion in section 10.5 of chapter 10 of this his free Corporate Finance textbook.

2 Multifactor Models

Another shortcoming of the CAPM is that it fails to explain the returns on portfolios formed on size (market capitalization) and value (book-to-market equity ratio), which we will explore in the practice notebook. These shortcomings have led to an explosion in multifactor models, which we will explore here.

2.1 The Fama-French Three-Factor Model

Fama and French (1993) expand the CAPM by adding two new factors to explain the excess returns on size and value. The size factor, SMB or small-minus-big, is a diversified portfolio that measures the excess returns of small market capitalization stocks over large market capitalization stocks. The value factor, HML of high-minus-low, is a diversified portfolio that measures the excess returns of high book-to-market stocks over low book-to-market stocks. We typically call this model the “Fama-French three-factor model” and express it as: \[E(r_i) - r_f = \alpha_i + \beta_{M} [E(r_M) - r_f)] + \beta_{SMB} SMB + \beta_{HML} HML\] There are two common uses for the three-factor model:

- Use the coefficient estimate on the intercept as a risk-adjusted performance measure. If \(\alpha_i\) is positive and statistically significant, we may attribute fund performance to manager skill.

- Use the remaining coefficient estimates to evaluate how the fund manager generates returns. Also, if the regression \(R^2\) is high, we may replace the fund manager with the factors themselves.

We can use the Fama-French three-factor model to evaluate Warren Buffett at Berkshire Hathaway (BRK-A). We will focus on the first three-years of easily available returns because Buffett had a larger edge when BRK was much smaller.

brk = (

yf.download(tickers='BRK-A')

.join(ff[0])

.rename(columns={'Mkt-RF': 'RM', 'RF': 'rf'})

.assign(

ri=lambda x: x['Adj Close'].pct_change().mul(100),

Ri=lambda x: x['ri'] - x['rf'],

rm=lambda x: x['RM'] + x['rf']

)

.rename_axis(columns='Variable')

)

brk.tail()[*********************100%%**********************] 1 of 1 completed| Variable | Open | High | Low | Close | Adj Close | Volume | RM | SMB | HML | rf | ri | Ri | rm |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||

| 2024-03-22 | 623558.0000 | 626334.0000 | 621121.0000 | 623040.0000 | 623040.0000 | 12800 | NaN | NaN | NaN | NaN | -0.3288 | NaN | NaN |

| 2024-03-25 | 622726.0000 | 625000.0000 | 617521.0000 | 619500.0000 | 619500.0000 | 16500 | NaN | NaN | NaN | NaN | -0.5682 | NaN | NaN |

| 2024-03-26 | 619805.0000 | 623790.0000 | 616716.0000 | 622380.0000 | 622380.0000 | 12700 | NaN | NaN | NaN | NaN | 0.4649 | NaN | NaN |

| 2024-03-27 | 625082.0000 | 630000.0000 | 621646.0000 | 629610.0000 | 629610.0000 | 12900 | NaN | NaN | NaN | NaN | 1.1617 | NaN | NaN |

| 2024-03-28 | 630365.0000 | 634800.0000 | 628150.0000 | 634440.0000 | 634440.0000 | 13100 | NaN | NaN | NaN | NaN | 0.7671 | NaN | NaN |

model = smf.ols(formula='Ri ~ RM + SMB + HML', data=brk.iloc[:756])

fit = model.fit()

summary = fit.summary()

summary| Dep. Variable: | Ri | R-squared: | 0.053 |

| Model: | OLS | Adj. R-squared: | 0.049 |

| Method: | Least Squares | F-statistic: | 13.91 |

| Date: | Fri, 29 Mar 2024 | Prob (F-statistic): | 7.81e-09 |

| Time: | 11:34:52 | Log-Likelihood: | -1208.9 |

| No. Observations: | 755 | AIC: | 2426. |

| Df Residuals: | 751 | BIC: | 2444. |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

| Intercept | 0.0801 | 0.044 | 1.809 | 0.071 | -0.007 | 0.167 |

| RM | 0.3484 | 0.075 | 4.643 | 0.000 | 0.201 | 0.496 |

| SMB | 0.4021 | 0.093 | 4.302 | 0.000 | 0.219 | 0.586 |

| HML | 0.0907 | 0.125 | 0.724 | 0.469 | -0.155 | 0.336 |

| Omnibus: | 118.864 | Durbin-Watson: | 1.797 |

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 1308.034 |

| Skew: | 0.284 | Prob(JB): | 9.20e-285 |

| Kurtosis: | 9.423 | Cond. No. | 3.51 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

The \(\alpha\) above seems small, but it is a daily value. We multiply \(\alpha\) by 252 to annualize it.

print(f"Buffet's annualized alpha in the early 1980s: {fit.params['Intercept'] * 252:0.4f}")Buffet's annualized alpha in the early 1980s: 20.1836We will explore rolling \(\alpha\)s and \(\beta\)s in the practice notebook using RollingOLS() from statsmodels.regression.rolling.

2.2 The Four-Factor and Five-Factor Models

There are literally hundreds of published factors! However, many of them have little explanatory power, in-sample or out-of-sample. Two more factor models with explanatory power, economic intuition, and widespread adoption are the four-factor model and the five-factor model.

The four-factor model adds a momentum factor to the Fama-French three-factor model. The momentum factor is a diversified portfolio that measures the excess returns of winner stocks over the loser stocks over the past 12 months. The momentum factor is often called UMD for up-minus-down or WML for winners-minus-losers. French stores the momentum factor in a different file because Fama and French are skeptical of momentum as a fundamental risk factor.

The five-factor model adds profitability and investment policy factors. The profitability factor, RMW or robust-minus-weak, measures the excess returns of stocks with high profits over those with low profits. The investment policy factor, CMA or conservative-minus-aggressive, measures the excess returns of stocks with low corporate investment (conservative) over those with high corporate investment (aggressive).

We will explore the four-factor and five-factor models in the practice notebook.